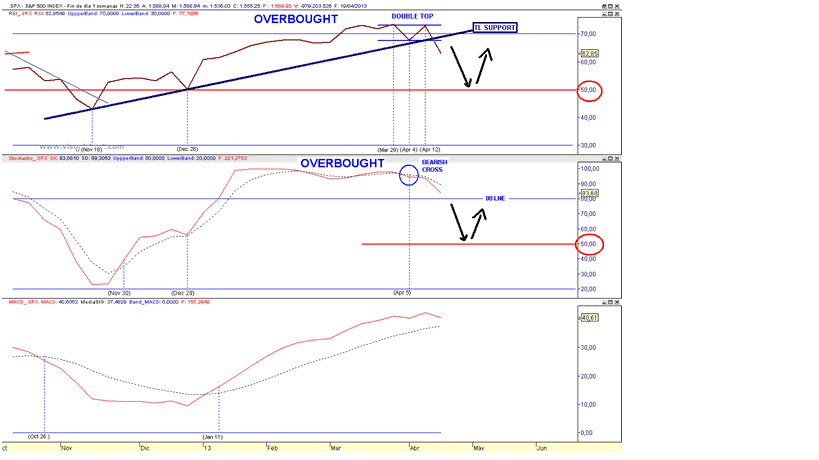

In my opinion the top of the up leg from the November lows is in place. We will have the absolute confirmation when price establishes a lower high. Below I show you the SPX weekly momentum indicators, where we can see that the RSI has breached the trend line support in force since the November 16 low. The next intermediate buy signal usually should occur when the RSI and the Stochastic retest the 50 line. I rule out a major reversal, instead I maintain the scenario of a retracement of the advance from the November lows. As I discussed last Friday the major reasons that suggest that price has not established a major top are: To become a subscriber, subscribe to our free newsletter services. Our service is free for all.

To become a subscriber, subscribe to our free newsletter services. Our service is free for all.

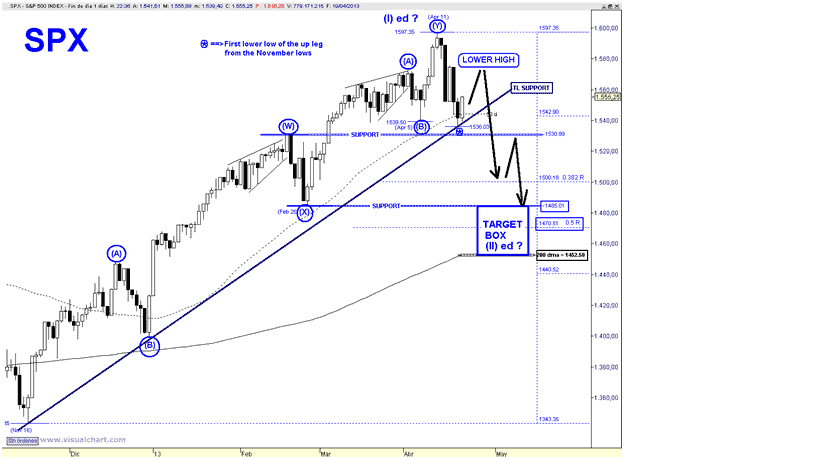

- The up leg from the November lows has unfolded a corrective 7-wave structure ===> A corrective EWP cannot establish a major Top.

- The current pullback is also unfolding a corrective pattern, ===> The intermediate trend remains up.

- Retails investors are extremely bearish (I have never seen a major top with an extremely low AAII Bull ratio)

To become a subscriber, subscribe to our free newsletter services. Our service is free for all.

To become a subscriber, subscribe to our free newsletter services. Our service is free for all. Continue reading

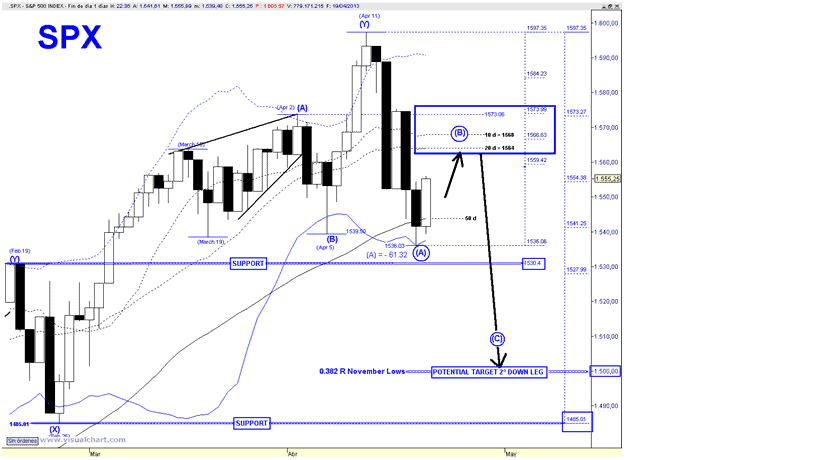

I MAINTAIN UNCHANGED THE CALL OF A TEMPORARY TOP

I MAINTAIN UNCHANGED THE CALL OF A TEMPORARY TOP