Unlock This Article

Unlock This ArticleOnly subscribers can read the full article. Please login to read the entire article.

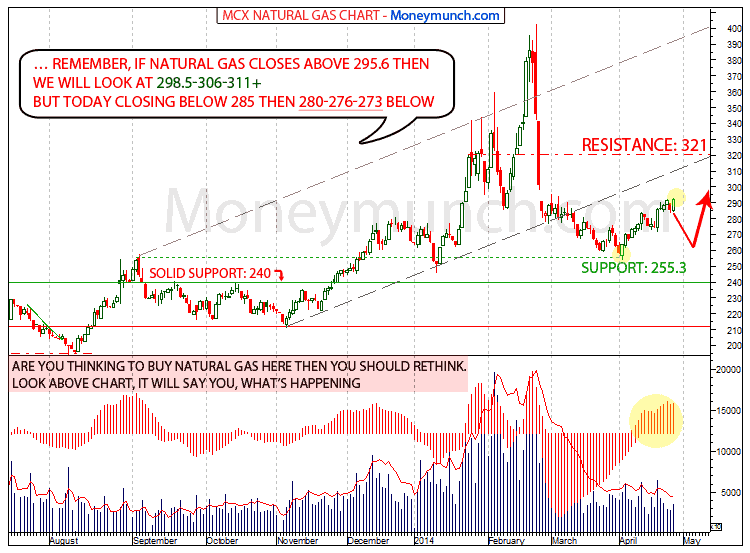

MCX MENTHAOIL – Trade Setup

Continue reading

Keep up with the latest breaking news and headlines from around the world with our comprehensive coverage of politics, business, technology, entertainment, and more. Stay informed and up-to-date with our news category.

The first case had confirmed in China Wuhan city. But the current state will give you a shock.

Last updated: April 08, 2020, 12:17 GMT

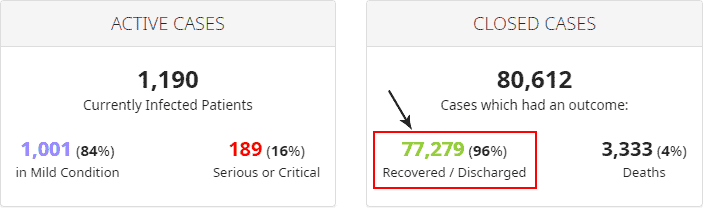

Coronavirus Cases: 81,802

Deaths: 3,333

Recovered: 77,279

The above state shows the situation is under control in China, and Wuhan city reopened. More

China Ends Wuhan Lockdown, but Normal Life Is a Distant Dream

Published April 7, 2020 | Updated April 8, 2020, 1:01 a.m. ET

By Raymond Zhong and Vivian Wang

– nytimes.com

“We began using them for disinfection and disease prevention,” said Hou Yongfei, deputy secretary-general of the Shanxi Province Unmanned Vehicle Association, the outlet reported, citing AsiaWire.

Wuhan recovery gives hope to rest of world, says WHO

All sectors of Indian financial markets are getting impacted by COVID-19. The total number of 123 countries are affected by a coronavirus. 1.32L+ confirmed cases and 4.9+ thousand people’s deaths reported by this virus.

All sectors of Indian financial markets are getting impacted by COVID-19. The total number of 123 countries are affected by a coronavirus. 1.32L+ confirmed cases and 4.9+ thousand people’s deaths reported by this virus.

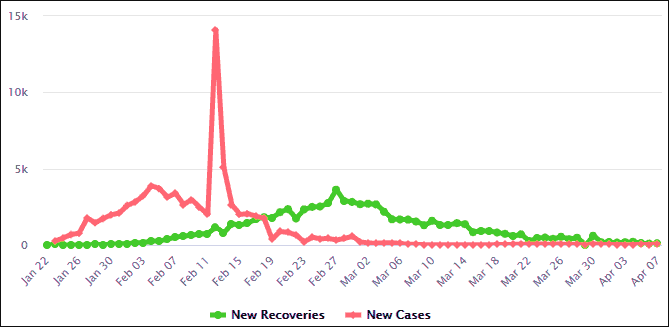

Data source: WHO (World Health Organization) & National Health Commission of the People’s Republic of China

Not only the Indian market, all over countries’ financial markets fear over this virus. It foothold is everywhere. But it will impact on a particular sector only. Many stocks & commodities will hit the bottom level. Isn’t it a new opportunity for smart traders? Don’t get scared. Don’t divert stocks from a portfolio without in-depth research. Fluctuation is temporary. It’s time for a new buying opportunity.

Hint: oil and manufacturing

To get the best stocks and commodities tips for investing in the current market situation, subscribe now.

Coronavirus information – India

The Helpline Number for coronavirus: +91-11-23978046

GST means Goods and Service Tax. Single Tax to promote Indian Trade and Industry.

A great step by Team India that will help transform the economy, bring in transparency and usher in the system of “one country one tax“.

The government clarified that the goods and services tax will keep its July 1st, 2017 date for countrywide rollout.

Our Government made it easy and completely online enrolment! All you need is a provisional ID, password, mobile number and email ID. Obtain your username/password by logging into www.aces.gov.in

For assistance: Call 1800 1200 232 or email: [email protected]

Revised Draft Model GST Law and Draft IGST Law available in public domain. The same can be accessed at www.cbec.gov.in, www.dor.gov.in or www.gst.gov.in

(Source: Central Board of Excise and Customs)

Dear Moneymunch valuable Readers,

GST will impact on many sectors of Indian Stock and Commodity Exchanges. Subscribe our premium services to get benefits from the impact of GST on exchanges securities.

Moneymunch going to launch Big Dhamaka Special Offers today and it will expire just a second ago before GST Launch! Limited members can enrol this offers and for enrolment write an email on [email protected].

Thank you!

Moneymunch Team

Just few hours back, Securities and Exchange Board of India announced unauthorized dairy investment scheme run by G N Dairies and has asked the company to refund investors’ money. Consequently, SEBI ordered 3-month time period from date of October 31 for return money to it investors because all investment schemes designed with wrong intention and company promise of high returns in the name of trading of cattle and ghee without obtaining requisite certificate from the market regulator.

If the company fails to comply with its directives, a reference would be made to the state government and local police to register a civil/criminal (consumer) case/complaints against them for fraud and cheating (cheater). – SEBIBy Moneymunch online investigation(review/feedback), the company claimed it has returned calves and ghee to as many as 45,000 investors.

Checkout similar two complaints investigated by Moneymunch:Continue reading

We know well, China natural gas production increasing in March to top in last two years and Gov. Data showed that natural gas utilization in China hit almost 170 billion cubic meters last year. United States domestic natural gas prices are falling by a lack of upward income stress.

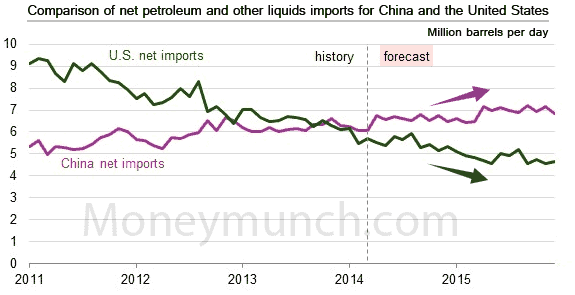

EIA (Energy information administrator) said, “China passed the United States as the world’s top importer of oil products.” If you don’t believe, look below chart with forecast:

As you can see China rising utilization and the United States’ short output “INSTANT STATIC REPORT” which creates by national development said same thing that from March 2013 natural gas production arrived at 11.2 billion cubic meter and U.S at 1.6 %.

The world’s biggest energy user wants a natural gas booming to speedy transformation in the U.S. and that’s the reason China has revolution envy.

To become a subscriber, subscribe to our free newsletter services. Our service is free for all.